Lease vs finance – Lease vs. finance is a crucial decision for acquiring assets, impacting both your finances and operations. Understanding the nuances of leasing versus traditional financing is key to making the right choice. This exploration delves into the financial, operational, and tax implications of each approach, equipping you with the knowledge to confidently navigate this complex landscape.

This guide examines the critical factors influencing lease versus finance decisions, including financial metrics, operational responsibilities, tax implications, and asset-specific considerations. We’ll also explore emerging trends in the market, equipping you to make informed choices.

Introduction to Lease vs. Finance

Choosing between leasing and financing an asset is a crucial financial decision, impacting a company’s cash flow and long-term strategy. This decision hinges on the specific needs and circumstances of the business, weighing the advantages and disadvantages of each option. Understanding the nuances of each approach is vital for informed financial planning.

Key Differences Between Leasing and Financing

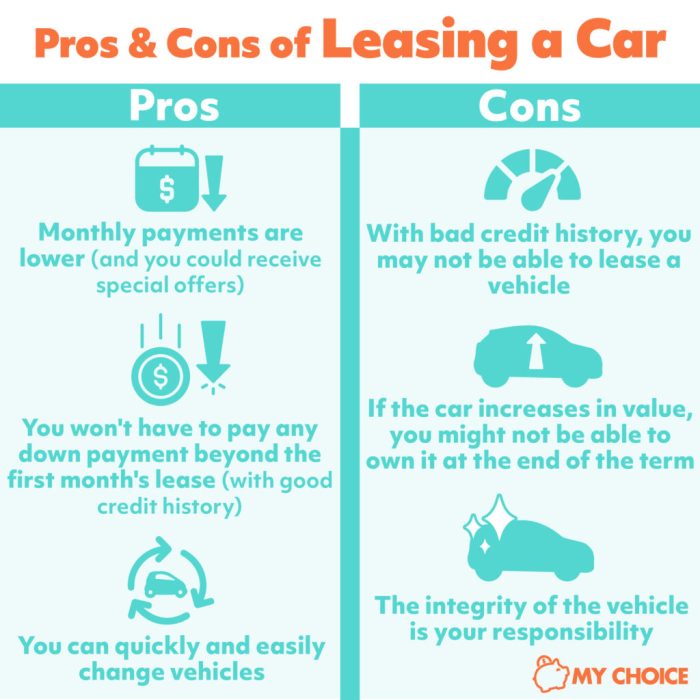

Leasing and financing differ fundamentally in how ownership and responsibility are handled. Leasing involves paying for the use of an asset, while financing involves acquiring ownership. In leasing, the lessee (the party renting the asset) doesn’t gain ownership, but retains the rights to use it. Conversely, financing, typically through loans, results in the borrower acquiring the asset.

Scenarios Where Lease vs. Finance Decisions Are Relevant

Lease vs. finance decisions are relevant in numerous business contexts. For example, a startup might lease equipment to minimize upfront costs and conserve capital, while a mature company might opt for financing to build long-term asset ownership and tax benefits. Companies in industries with rapidly evolving technology may find leasing more suitable, as it allows them to update their equipment more frequently.

Moreover, the availability of funding, the expected lifespan of the asset, and the company’s financial standing play significant roles in this decision.

Factors Influencing the Decision

Several key factors influence the choice between leasing and financing. These factors include the asset’s purchase price, the required upfront investment, the length of the lease or loan, the interest rate, and the projected usage of the asset over its operational lifespan.

Comparison of Leasing and Financing Options

| Feature | Leasing | Financing |

|---|---|---|

| Ownership | No ownership transfer | Ownership transfer |

| Upfront Costs | Potentially lower upfront costs | Higher upfront costs |

| Maintenance | Often included in lease agreements | Responsibility typically falls on the buyer |

| Tax Implications | Lease payments are often deductible as business expenses | Interest payments are deductible, but depreciation schedules vary |

| Flexibility | Greater flexibility to upgrade or replace assets | Less flexibility to upgrade assets mid-term |

| Residual Value | Potential residual value can be a factor in lease negotiations | Residual value is often not a major factor in financing |

| Risk | Less risk associated with obsolescence or unexpected repairs | Higher risk of obsolescence and potential financial strain from repairs |

This table provides a concise comparison of leasing and financing, highlighting the key distinctions. Businesses must carefully evaluate these features to make an informed decision that aligns with their specific needs and financial goals.

Financial Considerations

Deciding between leasing and financing often hinges on a meticulous analysis of financial metrics. Understanding the nuances of depreciation, interest payments, and tax implications, alongside the present value of cash flows, is crucial in making an informed choice. This section delves into the key financial aspects of each option, providing a framework for comparison.

Key Financial Metrics

Different financial metrics are employed to assess the economic viability of leasing versus financing. These metrics help quantify the associated costs and benefits of each approach. Critical factors include the total cost of ownership (TCO), the net present value (NPV), and the internal rate of return (IRR). Each metric provides a unique perspective on the financial implications of a particular option.

Depreciation

Depreciation plays a significant role in the financial evaluation of assets. In a financing scenario, depreciation reduces the taxable income over the asset’s lifespan, leading to tax savings. Leasing, on the other hand, does not typically involve the recognition of depreciation on the balance sheet of the lessee. This distinction impacts the overall financial burden of each approach, influencing the decision-making process.

Interest Payments

Interest payments are a substantial component of financing costs. The interest rate and loan term directly affect the total interest expense incurred. Lease payments, while seemingly fixed, may incorporate implicit interest charges. Understanding the specific structure of interest payments and their impact on the overall cost is critical in evaluating the financing option. A comparison of interest expenses is essential for an accurate assessment.

Tax Implications

Tax implications differ significantly between leasing and financing. In financing, depreciation deductions and interest payments can lead to substantial tax savings. Leasing structures may offer tax advantages in specific scenarios, particularly regarding the treatment of lease payments. Tax codes and regulations vary by jurisdiction, impacting the final financial outcome. Therefore, careful consideration of the applicable tax laws is paramount.

Present Value of Cash Flows

The present value of cash flows (PV) is a crucial tool for evaluating lease vs. finance decisions. It accounts for the time value of money, ensuring that future cash flows are discounted to their present worth. This allows for a direct comparison of the net present value of the lease and finance options, providing a consistent evaluation framework.

Using a discount rate, often the company’s cost of capital, the present values of future payments are calculated.

Present Value = Future Value / (1 + Interest Rate)^Number of Periods

Example Calculation: Lease Payments

Let’s consider a $50,000 asset with a 5-year lease at a 5% annual interest rate. Using appropriate financial calculators or software, the monthly lease payment would be approximately $X. Adjusting the interest rate, term, or asset value will change the lease payment.

Example Calculation: Loan Payments

For a $50,000 loan with a 5-year term and a 5% annual interest rate, the monthly loan payment would be approximately $Y. Adjusting the interest rate, term, or loan amount will alter the monthly payment.

| Factor | Lease | Finance |

|---|---|---|

| Initial Investment | Lower | Higher |

| Monthly Payments | Fixed | Variable (typically) |

| Tax Deductions | Potentially lower | Potentially higher |

Operational Considerations

Understanding the operational implications of leasing versus financing is crucial for making an informed decision. Both methods affect a company’s day-to-day activities, impacting responsibilities, maintenance, and overall flexibility. This section delves into the key operational differences between leasing and financing.Operational responsibilities differ significantly between lessees and borrowers. Lessees generally have fewer operational responsibilities, while borrowers bear a greater burden in managing and maintaining the asset.

Lessee Operational Responsibilities

The lessee, under a lease agreement, typically focuses on utilizing the asset. Specific responsibilities are Artikeld in the lease contract. These might include operating the asset within agreed-upon parameters, ensuring compliance with applicable regulations, and managing the asset’s day-to-day use. Examples include adhering to safety standards or maintaining records of usage. The lease agreement usually specifies the lessee’s obligations, which could range from simple operational procedures to complex regulatory compliance.

Borrower Operational Responsibilities

Conversely, the borrower (under a financing agreement) assumes a broader range of operational responsibilities. This includes overseeing the asset’s maintenance, repairs, and insurance, as well as complying with any applicable regulations and industry standards. The borrower is fully responsible for the asset’s upkeep and operational integrity, unlike a lessee who has limited responsibility in this area.

Maintenance and Repair Responsibilities

Maintenance and repair responsibilities are a key distinction. Lease agreements often clearly define who is responsible for these tasks. Commonly, the lessee is responsible for routine maintenance, while the lessor (owner of the asset under lease) handles major repairs. The lease contract specifies the extent of these responsibilities, from basic upkeep to comprehensive repairs.

Impact of Lease Terms on Operational Flexibility

Lease terms significantly impact operational flexibility. Long-term leases often restrict the lessee’s ability to adjust operations or change equipment, while shorter-term leases offer more operational agility. This difference can be critical for businesses with evolving needs or those in dynamic industries. A company seeking quick adaptation would likely prefer a shorter-term lease or a financing option with more flexibility.

Types of Lease Agreements and Operational Implications

Different lease agreements have varying operational implications. Understanding these nuances is vital for strategic decision-making.

| Lease Type | Operational Implications |

|---|---|

| Operating Lease | Lessee has limited responsibilities; lessor handles maintenance and repairs. Generally, higher operational flexibility. |

| Finance Lease | Lessee assumes more operational responsibilities, often including maintenance and repair. Less operational flexibility compared to operating leases. |

| Sale and Leaseback | A complex transaction; lessee effectively sells an asset and then leases it back. Operational responsibilities often depend on the specifics of the agreement. |

Tax Implications

Understanding the tax implications of leasing versus financing is crucial for making an informed decision. Tax laws can significantly impact the overall cost of each option, and these implications vary based on the specific circumstances of the business or individual. Different depreciation schedules and tax treatments of lease payments versus loan payments can dramatically alter the financial outcome.The tax code often favors one method over the other, making a thorough analysis essential.

The choice between leasing and financing is not solely based on initial costs; the long-term tax advantages and disadvantages play a pivotal role.

Tax Advantages of Leasing

Lease payments are typically considered business expenses, directly reducing taxable income. This immediate tax deduction can lead to substantial savings in the short term. Furthermore, the lessee isn’t burdened with the depreciation expense. The lessor handles this, which can simplify the financial reporting process.

Tax Disadvantages of Leasing

While lease payments offer immediate tax benefits, some leases might be structured in a way that classifies them as capital leases, which are treated more like purchases for tax purposes. This can result in a reduction of the tax benefits and may require accounting for depreciation over the asset’s life.

Tax Advantages of Financing, Lease vs finance

Financing, on the other hand, allows for depreciation deductions over the asset’s life. This allows for a more gradual reduction in taxable income over the loan’s duration. This can be particularly advantageous for businesses and individuals in higher tax brackets.

Tax Disadvantages of Financing

Interest payments on loans are also tax-deductible, reducing taxable income. However, the initial investment and the loan amount are not tax-deductible. This means the full cost of the asset is not immediately offset, in contrast to the immediate tax benefit of lease payments.

Choosing between leasing and financing an EV often hinges on factors like the specific vehicle’s range. Considering the range comparison for different electric vehicles is crucial before making a decision. EV range comparison can help you assess how far your chosen EV can travel on a single charge, which ultimately impacts your lease vs. finance calculations.

Ultimately, the best approach to EV ownership depends on personal driving needs and budget.

Tax Treatment of Lease Payments (Businesses)

Lease payments for businesses are generally treated as operating expenses, reducing taxable income in the year they are incurred. The specific tax treatment depends on the lease’s classification as an operating lease or a capital lease. Capital leases are often treated more like purchases, with depreciation deductions over the asset’s life.

Tax Treatment of Loan Payments (Businesses)

Loan payments for businesses include both principal and interest components. Interest payments are typically deductible, reducing taxable income, while principal payments do not directly impact taxable income.

Tax Treatment of Lease Payments (Individuals)

For individuals, lease payments are typically treated as operating expenses, reducing taxable income. Similar to businesses, the tax treatment can vary depending on the lease classification. Personal property taxes, if applicable, may be deducted separately.

Tax Treatment of Loan Payments (Individuals)

Similar to businesses, loan payments for individuals have both principal and interest components. Interest payments are deductible, reducing taxable income, while principal payments do not directly affect taxable income.

Depreciation Schedules and Tax Liability

Different assets have varying depreciation schedules under tax laws. The chosen method significantly impacts the tax liability over the asset’s life. Straight-line depreciation, accelerated depreciation methods (like the declining balance method), and MACRS (Modified Accelerated Cost Recovery System) are common options, each affecting the timing and amount of tax deductions.

Impact of Tax Laws on Lease vs. Finance Choice

Tax laws significantly influence the optimal choice between leasing and financing. The timing and amount of tax deductions, as well as the asset’s classification (operating or capital lease), are key factors. Consult with a tax professional to assess the specific tax implications of a lease or financing agreement in your situation. Tax laws are complex and vary by jurisdiction, so tailored advice is essential.

Asset-Specific Considerations

Choosing between leasing and financing an asset involves a nuanced evaluation, critically dependent on the asset’s unique characteristics. Different assets present varying advantages and disadvantages for each financing option, impacting the overall cost and operational implications. This section explores how the specifics of an asset influence the optimal financing strategy.Understanding the interplay between asset value, useful life, and market conditions is crucial for a sound decision.

The specific financial and operational characteristics of high-value assets or assets with unique operational requirements will also be highlighted.

Impact of Asset Value

Asset value significantly impacts the lease vs. finance decision. High-value assets often favor financing due to the potential for greater tax benefits and depreciation deductions. Conversely, low-value assets might lean towards leasing, which can simplify the process and reduce upfront capital expenditure. Consider a high-value piece of equipment, say, a specialized manufacturing machine.

Financing this equipment, with the option to depreciate its value, could prove more beneficial for tax purposes than leasing it.

Influence of Asset Useful Life

The asset’s useful life is a key factor. Assets with a short useful life might be better suited for leasing, reducing the financial burden of owning the asset over its entire lifespan. In contrast, long-term assets often benefit from financing, allowing for depreciation and potential tax advantages over a more extended period. For instance, a fleet of delivery trucks with a projected operational life of 5 years might be better suited for leasing, while a manufacturing facility, expected to remain operational for 20 years, would more likely benefit from financing.

Effect of Market Conditions

Market conditions play a substantial role. Fluctuating market values for specific assets could affect the lease vs. finance decision. If market values are anticipated to increase significantly during the asset’s lifespan, financing might offer a better option. If values are expected to decrease or if the market is volatile, leasing could offer greater flexibility and less financial risk.

For example, during a period of high inflation, financing an asset might prove more advantageous due to the potential for inflation-adjusted depreciation deductions.

Asset-Specific Lease vs. Finance Structures

Various lease vs. finance structures exist, tailored to the characteristics of particular assets. For example, specialized manufacturing equipment might necessitate a financing structure with customized depreciation schedules to reflect its unique operational needs. Similarly, a fleet of vehicles might be better served by a lease agreement that includes maintenance and repair coverage.

| Asset Type | Typical Lease vs. Finance Structure |

|---|---|

| Specialized manufacturing equipment | Financing with customized depreciation schedules |

| Fleet of vehicles | Lease agreement with maintenance and repair coverage |

| Real estate | Financing with loan amortization schedules |

High-Value Asset Considerations

High-value assets demand meticulous analysis. Factors like the asset’s specific operational requirements and projected return on investment should be evaluated alongside financial considerations. A high-value asset, like a cutting-edge research facility, might necessitate a customized financing plan that accounts for potential research breakthroughs and the facility’s unique operational demands.

Assets with Unique Operational Requirements

Assets with unique operational requirements deserve special attention. For instance, a piece of equipment requiring specialized maintenance or a unique operating environment might necessitate a lease structure that covers those needs. Consider a piece of equipment requiring specialized maintenance or unique operating environment. This asset might require a lease structure that accounts for those specific needs.

Risk Assessment

A critical aspect of evaluating lease versus finance options is understanding the inherent risks associated with each approach. Careful consideration of potential pitfalls, such as obsolescence, market fluctuations, and maintenance costs, is essential for making an informed decision. This section delves into these risks and Artikels strategies for mitigating them.

Lease Risks

Leasing, while often perceived as a more flexible option, carries its own set of risks. A key risk is the potential for the leased asset to become obsolete before the lease term ends. This could render the asset less valuable or even unusable, leading to financial losses. Market fluctuations can also impact the value of leased assets.

If the market value declines significantly, the lessee may be stuck with an asset worth less than the lease payments. Furthermore, unexpected maintenance costs can significantly impact the overall cost of leasing. These costs can be unpredictable and potentially substantial.

Finance Risks

Financing, though often perceived as a more stable approach, also presents specific risks. The risk of obsolescence is still present, though less pronounced in the short term, as the asset is owned. Market fluctuations can impact the resale value of the financed asset, especially in industries with volatile market conditions. For example, a significant downturn in the automotive industry could drastically reduce the resale value of a newly purchased vehicle.

Moreover, the financial obligations associated with financing, such as loan repayments and interest payments, can create significant financial strain if not properly accounted for.

Obsolescence Risk Mitigation

To mitigate obsolescence risk, thorough research into the asset’s projected lifespan and technological advancements is crucial. This involves analyzing industry trends, consulting with experts, and identifying potential replacements. For example, if a company is considering leasing a piece of specialized equipment, understanding the typical lifespan of similar equipment in the market and potential technological advancements in the field can help them assess the obsolescence risk.

Market Fluctuation Risk Mitigation

Market fluctuations can be mitigated by careful market analysis and forecasting. Companies can consider the potential for market downturns and the impact on asset values. Diversification of assets can also be a helpful strategy.

Maintenance Cost Risk Mitigation

Proactive maintenance strategies and detailed cost estimations can help mitigate the risk of unexpected maintenance costs. Implementing a preventative maintenance schedule and obtaining quotes from multiple service providers can provide valuable insights. Consideration of extended warranties or service contracts can also be helpful in mitigating this risk.

Impact of Unforeseen Circumstances

Unforeseen circumstances, such as natural disasters, pandemics, or economic crises, can significantly impact both leasing and financing decisions. The impact of such events is highly variable and dependent on the specific nature of the circumstance and the industry. For example, the COVID-19 pandemic significantly impacted the travel industry, leading to a substantial decrease in demand for aircraft, which, in turn, impacted leasing and financing decisions.

Companies should have contingency plans in place to address such situations.

Decision-Making Process

A structured approach to evaluating lease versus finance options is crucial for informed business decisions. Choosing the right financing method significantly impacts cash flow, tax obligations, and overall profitability. This section details a step-by-step process for making informed decisions, outlining key factors to consider at each stage.Evaluating financing options requires a systematic process. This process involves assessing various factors to ensure the chosen method aligns with the company’s financial goals and operational needs.

The process will be demonstrated with a case study example.

Defining Objectives and Requirements

Clearly defining the business objectives and specific needs is the first step. This involves understanding the purpose of the asset acquisition, its intended use, and the anticipated lifespan. This initial stage requires a thorough analysis of the company’s strategic plans and the role the asset will play in achieving these plans. Identifying the specific features, capacity, and technical specifications needed for the asset is also crucial.

Gathering Financial Data

Gathering relevant financial data is essential for comparing lease and financing options. This includes projected revenue, operating costs, and existing debt levels. Detailed financial statements and cash flow projections will inform the analysis and facilitate accurate comparisons between leasing and financing options. Key financial metrics, like projected ROI and payback periods, are calculated to evaluate the financial implications of each choice.

Evaluating Lease and Financing Options

Thorough analysis of both lease and financing options is necessary. This involves scrutinizing lease terms, including lease payments, residual value guarantees, and maintenance provisions. For financing options, the assessment includes loan terms, interest rates, repayment schedules, and associated fees. Each financing option should be assessed based on its cost, structure, and implications for the company’s financial health.

Assessing Operational Implications

Considering the operational implications of each financing option is vital. This includes evaluating the asset’s integration into existing operations, required maintenance schedules, and potential impact on workforce needs. Operational feasibility and potential disruption to daily workflows should be carefully considered during the assessment.

Tax Analysis and Implications

A detailed tax analysis of both lease and financing options is critical. Tax implications of each financing option, including deductions and tax credits, should be examined in detail. This involves consulting with tax professionals to ensure accurate calculation of tax benefits and obligations for each scenario.

Risk Assessment and Mitigation

Identifying and mitigating potential risks associated with each financing option is essential. This involves assessing potential market fluctuations, technological obsolescence, and regulatory changes that might affect the asset’s value. Strategies for risk mitigation, contingency plans, and insurance considerations are also examined to safeguard the company’s investment.

Decision-Making and Implementation

Based on the comprehensive analysis of financial, operational, and tax implications, a final decision is made. This involves weighing the pros and cons of each option, considering the company’s overall financial position, and selecting the option that best aligns with the business’s goals. A documented decision-making process, including rationale and justifications, is crucial for future reference and accountability.

Case Study Example

A company, “Tech Solutions Inc.”, needs a new high-speed 3D printer for product development. They can either lease or finance the printer. Their financial projections show a strong ROI over the next three years, but they also face potential obsolescence in five years. After careful analysis, the lease option, with its lower upfront cost and flexibility, proves the best option, mitigating the risk of obsolescence.

The decision is documented and the lease agreement is signed.

Case Studies

Analyzing real-world scenarios provides valuable insights into the effectiveness and challenges of lease versus finance decisions. These case studies demonstrate how factors like industry, asset specifics, and financial considerations interact to influence outcomes.

Successful Lease vs. Finance Decision

A successful lease vs. finance decision often hinges on a comprehensive evaluation of short-term and long-term financial implications, combined with a deep understanding of the specific asset’s value and operational needs. A software company, for instance, recognized the benefits of leasing servers instead of purchasing them outright.

- Reduced upfront capital expenditure: Leasing allowed the company to allocate capital to other core business functions, such as research and development or marketing initiatives, without compromising their ability to acquire necessary technology. This freed up significant funds for growth.

- Flexibility and scalability: As the company’s server needs evolved, the lease terms allowed for adjustments in capacity without incurring the costs and complexities of purchasing new equipment.

- Reduced maintenance and support burden: The leasing agreement often includes maintenance and support, thereby reducing the company’s internal workload and allowing them to concentrate on their core business.

The outcomes were a more agile response to market demands, improved cash flow, and a direct impact on operational efficiency, demonstrating how leasing enabled a more streamlined approach to technological investment.

Unsuccessful Lease vs. Finance Decision

A manufacturing company’s decision to lease a complex piece of machinery instead of financing its purchase proved less successful.

- Unexpected maintenance costs: The lease agreement, while including maintenance, did not cover certain specialized repairs that became necessary due to the machinery’s intricate design. This significantly exceeded the anticipated costs, negatively affecting the company’s budget.

- Limited operational flexibility: The lease terms restricted the company’s ability to modify or upgrade the equipment based on evolving production needs. This constraint hindered the company’s efforts to optimize production processes and adapt to changing market demands.

- Lack of ownership and potential resale value: Not owning the equipment limited the company’s potential future value, as it could not benefit from a potential resale of the asset if market conditions were favorable. This impacted their long-term strategic options.

The company’s initial analysis, while comprehensive, overlooked the intricacies of the machinery’s maintenance requirements and the lease’s limitations on operational flexibility. The outcome underscored the importance of a thorough assessment of potential maintenance expenses and lease restrictions to ensure the decision aligns with the long-term operational strategy and potential financial benefits.

Deciding between leasing and financing a vehicle is a key consideration. Current auto trends, like the increasing popularity of electric vehicles, are influencing these choices. For instance, Auto trends are pushing manufacturers to offer more attractive leasing options for these eco-friendly cars. Ultimately, the best choice for lease vs finance remains dependent on individual circumstances and financial goals.

Emerging Trends: Lease Vs Finance

The lease vs. finance landscape is constantly evolving, driven by technological advancements and shifting regulatory environments. Understanding these trends is crucial for businesses to make informed decisions and optimize their financial strategies. This section explores current and potential future developments in the market.

Technological Advancements

Technological advancements are fundamentally reshaping the lease vs. finance process. Digital platforms are streamlining the entire lifecycle, from initial assessment to ongoing management of leased or financed assets. This includes automated valuations, faster contract processing, and improved tracking of asset performance. Furthermore, AI and machine learning are playing an increasing role in optimizing lease terms and identifying potential risks.

This improved efficiency can lead to reduced costs and faster turnaround times for transactions.

Evolving Regulations

Regulatory changes can significantly impact lease vs. finance decisions. Governments worldwide are continuously updating accounting standards, tax laws, and environmental regulations. These changes may affect the tax implications of leasing versus financing, potentially altering the cost-benefit analysis for different types of assets. Understanding these regulatory shifts is essential for compliance and strategic planning.

New Financial Instruments

Innovative financial instruments are emerging to cater to specific needs in the lease vs. finance market. One notable trend is the development of green financing options for environmentally friendly assets. These specialized instruments aim to promote sustainable practices by providing favorable financing terms for eco-conscious investments. Furthermore, asset-backed securities and other structured finance solutions are being explored to enhance the liquidity and marketability of lease portfolios.

Future Developments

The future of lease vs. finance is likely to be characterized by increased automation, greater transparency, and enhanced risk management capabilities. Greater use of blockchain technology could further enhance security and traceability in the lease lifecycle. The rise of the sharing economy and subscription models may also influence the future of asset acquisition, potentially leading to alternative financing structures for businesses.

This could result in more flexible and dynamic solutions for acquiring assets, aligning with evolving business models.

Ultimate Conclusion

In conclusion, the choice between leasing and financing depends on a variety of factors, including the specific asset, your financial situation, and your operational needs. Careful consideration of the financial metrics, operational implications, and tax implications is crucial to making an informed decision. This guide provides a comprehensive overview, equipping you with the tools and insights necessary to confidently navigate the complexities of lease versus finance decisions.

FAQ Section

What are the key differences between leasing and financing?

Leasing typically involves paying periodic payments for the use of an asset, without ownership. Financing, on the other hand, involves borrowing money to purchase the asset, ultimately transferring ownership to the borrower.

How does depreciation impact lease vs. finance decisions?

Depreciation impacts the tax implications of both leasing and financing. Leasing often avoids the immediate depreciation expense, while financing allows for depreciation deductions over the asset’s lifespan. This affects the net cost of each option.

What are some common operational responsibilities under a lease agreement?

Operational responsibilities vary depending on the lease terms. This may include maintenance, repairs, insurance, and other ongoing operational costs.

How do tax laws influence the choice between leasing and financing?

Tax laws can significantly affect the net cost of each option. Deductions for depreciation and interest payments can vary, leading to different tax burdens for each approach.